Add Row

Add Row  Add

Add

Understanding the Fraud Triangle: A Crucial Framework for Small Businesses

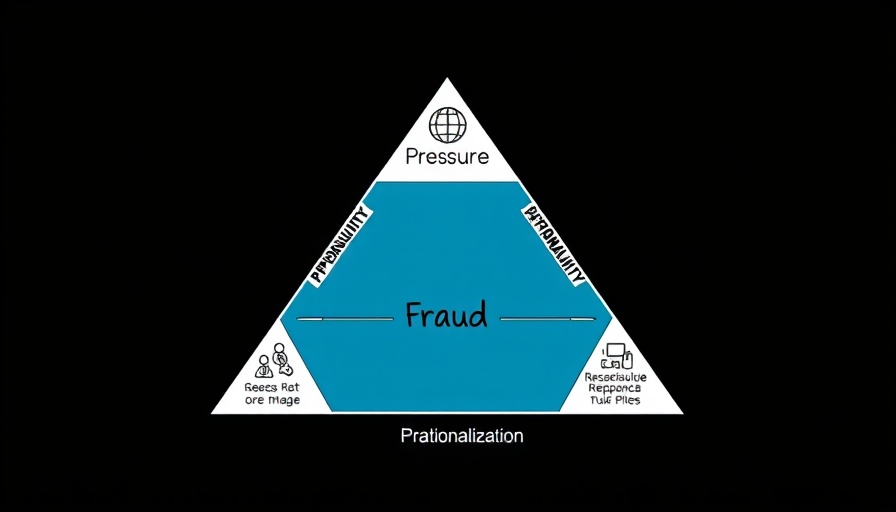

The fraud triangle is a critical tool that small business owners must understand to safeguard their enterprises from occupational fraud. Developed by criminologist Donald R. Cressey, this framework identifies three essential components—pressure, opportunity, and rationalization—that together create a fertile ground for fraud to occur within organizations.

Pressure: The Incentive Behind Fraud

At the heart of the fraud triangle is pressure, which encompasses the financial or emotional motives that might push a trusted employee towards committing fraud. Common pressures include financial emergencies, lifestyle affluence, or even workplace frustrations. For instance, an employee facing unexpected medical expenses may feel tempted to embezzle funds to alleviate stress. Recognizing these pressures is fundamental in creating preventive measures for fraud.

Opportunity: Control What You Can

Unlike pressure and rationalization, opportunity is an element that business owners can significantly control. This component refers to the ability employees have to perpetrate fraud without getting caught. Weak internal controls, lack of supervision, and inadequate oversight create openings for fraud. Business owners can mitigate these risks by implementing robust checks and balances, such as separation of duties and regular audits—a proactive stance that can deter potential fraudsters.

Rationalization: How Employees Justify Their Actions

The third leg of the fraud triangle, rationalization, pertains to the internal justifications employees make for their dishonest actions. For many, committing fraud can be rationalized through thoughts like, ‘I deserve this’ or ‘they won't miss that money.’ By fostering a transparent work environment with clear ethical guidelines, business owners can diminish these justifications, ensuring that employees understand their accountability within the organization.

Implementing Effective Fraud Prevention Strategies

Awareness of the fraud triangle's components can empower small business owners to develop an effective fraud prevention plan. It's essential to establish a culture of open communication, empathy, and realistic performance expectations that decrease the likelihood of fraud. Strategies may include offering employee assistance programs, integrating strong internal controls, and creating a supportive workplace atmosphere that discourages the feeling of isolation.

Your Action Plan Against Fraud

Recognizing the influences behind occupational fraud is paramount, but taking actionable steps is what truly protects your business. Beyond understanding the fraud triangle, small business owners should actively engage with their employees, implement stringent controls, and foster a positive workplace culture. By doing so, they can prevent fraud before it begins, ensuring the integrity and long-term success of their organization.

Write A Comment